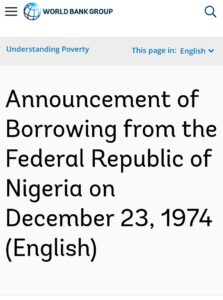

There was a time when Nigeria was so flush with cash that international institutions came to it for money. It sounds impossible today, but in 1974 the World Bank borrowed from Nigeria at the height of the oil boom.

In 1974 the World Bank borrowed approximately 240 million dollars from Nigeria.

The 1973 Yom Kippur War triggered a global oil crisis. Crude oil prices quadrupled almost overnight, and oil-exporting countries saw their revenues explode.

Nigeria’s treasury filled with petrodollars. Head of State General Yakubu Gowon famously said Nigeria’s problem was not money, but how to spend it.

The World Bank took Nigeria’s surplus and used it to fund development projects in poorer, oil-importing nations that were struggling with high energy costs.

It was a brief moment when the financial flow reversed. Instead of Nigeria going to Washington for a loan, Washington’s institutions were tapping Lagos.

That oil wealth funded more than domestic projects. Nigeria became a major backer of African liberation. It gave heavy financial support to the anti-apartheid movement in South Africa, and to liberation movements in Angola, Mozambique, and Zimbabwe.

Britain relied heavily on Nigerian oil, and Nigeria held massive sterling reserves in London banks. Those reserves helped keep the British Pound stable at the time.

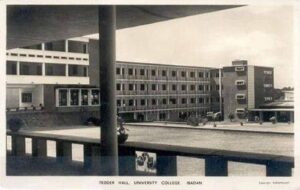

This was also a golden age for education. The University of Ibadan and the University of Ife were considered world-class. They attracted professors and students from across Asia, Europe, and Africa. Nigerian degrees carried weight internationally.

The Onset of Decay and The Fall

The boom did not last. Economists call what happened next Dutch Disease. Nigeria abandoned its productive agricultural sectors, groundnuts, cocoa, and palm oil, to depend almost entirely on crude oil.

Spending became unchecked. The government launched massive infrastructure projects, many with little planning, and hosted expensive cultural events like FESTAC 77. Reserves were drained quickly.

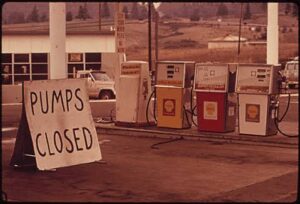

Then the price shock came. In the early 1980s global oil prices collapsed. A mono-economy built on one commodity could not survive it. Revenue fell, debts rose, and foreign exchange dried up.

In 1986, under General Ibrahim Babangida, Nigeria entered an IMF Structural Adjustment Program. The Naira was devalued massively. Inflation spiked. Subsidies were cut. Factories that depended on imported inputs closed. Professionals left the country in what became known as the brain drain. Teachers, doctors, engineers, and academics moved abroad for better pay and stability.

Nigeria’s story is now taught as a cautionary tale about resource mismanagement. Oil created instant wealth, but without diversification, savings, and strong institutions, the wealth disappeared just as fast.

Yet the foundation of the country has shifted. The new wealth is less about barrels and more about people. Nigeria today has Africa’s largest creative economy. Nollywood and Afrobeats reach audiences worldwide. The tech ecosystem in Lagos and other cities is producing startups, fintech, and digital jobs at a pace that rivals anywhere on the continent.

The irony is clear. In 1974 the World Bank borrowed from Nigeria because it had more money than ideas. Fifty years later, Nigeria has more ideas and talent than money, and is still trying to build governance to match the drive of its citizens.

The mighty fell not because the potential vanished, but because the economy was built on one price, one product, and one bet. The question now is whether that same potential can be turned into lasting prosperity….See_More

")

")

")

Leave a Reply